Just a few years ago, media executives thought theatrical releases didn’t benefit their streaming services. Now, many of them think the opposite.

For much of the past decade, Hollywood executives striving to catch Netflix started believing that the only way to increase the subscriber numbers for their own streaming services was either by significantly narrowing the time between a film’s theatrical release and its appearance on streaming or by putting both out simultaneously.

But the industry has now largely come to a very different conclusion: The key to making a movie a streaming success and attracting new subscribers is to first release it in theaters.

Especially since the pandemic, this “user obsession” has driven tech-minded folks at streamers to demand that movies be released day-and-date on streaming services. “Consumer preferences” — that people should be able to watch anything whenever they want, wherever they way — dogmatically drove this agenda.

But beyond customers asking for it in surveys, there’s no evidence that this makes business sense or actually caters to the customer. The theatrical hype machine and word of mouth is part of wanting to watch something in the first place. I wrote about this in 2017 when Disney first hinted at day-and-date. No amount of streaming marketing can buy theatrical’s inherent offering: placing a movie into thousands of multiplexes across America. It’s like instantly scaling an experiential event into 5000 cities. Why pass that up?

Now imagine you’re Disney or Universal and you actually rely not just on streaming (like the example in this article, Amazon’s original “Red One”) but need to be able to sell derivative merch, products, games and parks tickets for years into the future. You need a red carpet and a theatrical release to launch the multi-year momentum required for that kind of lasting IP.

I recently resurrected an old presentation I gave at Twitch and shared a new version with students in Justin Winter‘s AI Producing class at LMU. This post is a recap!

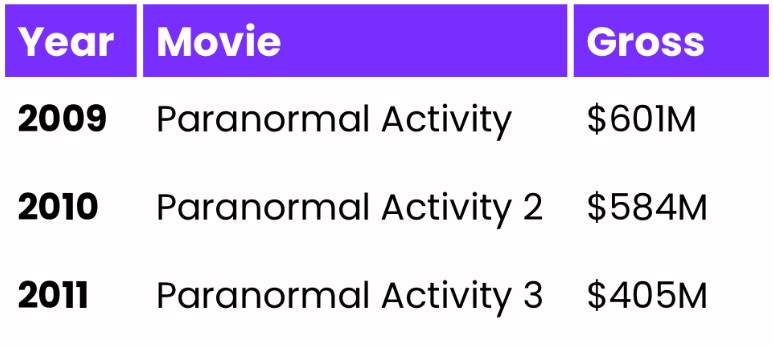

15 years ago, Paranormal Activity was released, just in time for Halloween in 2009. It was a viral phenomenon and the highest grossing horror movie of the year. The momentum was so powerful that Paranormal 2 and 3 became the highest grossing horror films in 2010 and 2011.

This was an industry-shifting movie for many reasons (the beginning of Blumhouse’s low-budget model and the marketing campaign1 among them), but I want to focus on one unexpected upshot you won’t see unless you dig into the data like I have: Paranormal Activity met very unique conditions in the market which caused a new genre to emerge. It’s a case study in how niche content can go mainstream…and how sometimes, it doesn’t.

PA was originally made for just $15,000 as a “found footage” horror movie. The premise is that we’re viewing “real” home video footage of an event that has been edited together after the fact. This masterful style gives the film creative license to have all the warts and imperfections which come with something user-generated. The low budget made it outrageously profitable. PA appeared in film festivals in 2007. It was scooped up by Paramount for only $350,000, who invested another $200,000 and widely released it in 2009, earning $601M (a phenomenal 1000x ROI for Paramount).

Highest Grossing Horror Films by Year: 2009-2011

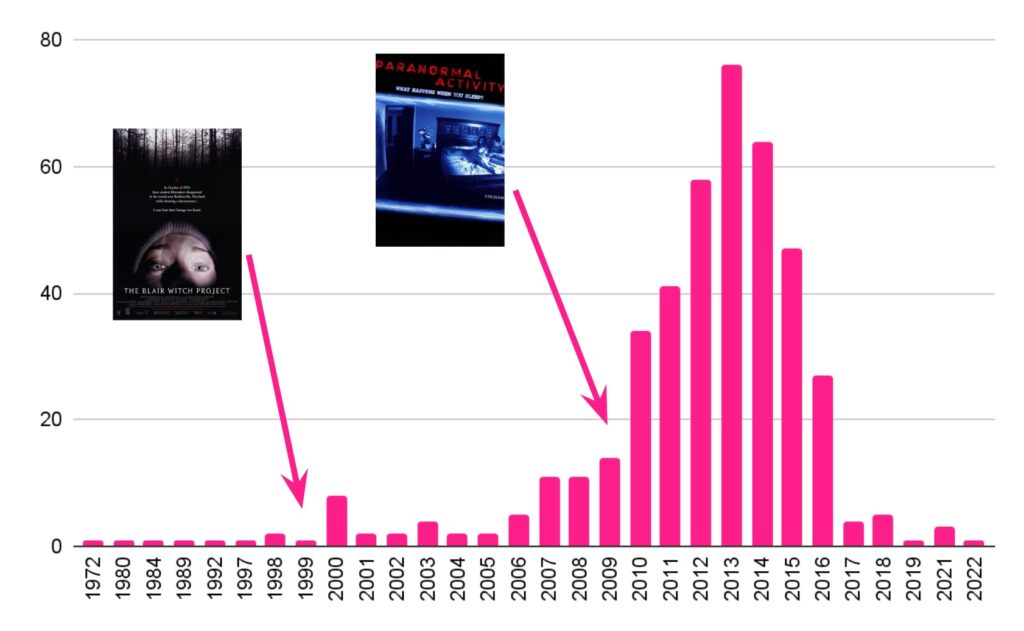

That’s all great for the individual franchise. But it’s even better for the film community because it kickstarted a new genre. Right after after PA comes out (2007 in festivals, 2009 wide release), independent filmmakers and major studios began creating hundreds of new found-footage horror movies. Have a look at this data I pulled from IMDb, charting the number of found footage horror movies since the 70s:

Number of Found Footage Horror Movies Released per Year

As you can see, >80% of all found footage horror was made after PA. Why? Because PA helped people clearly see the template for this content: do away with high-cost talent, lighting, music, production value – don’t even invest in visual effects and gore. It conveyed a formula for the genre which others copied.

You’re probably already getting ahead of me though… why am I giving all this credit to Paranormal Activity? There’s one more bump on this graph.

Indeed, 10 years prior, The Blair Witch Project debuted. But only a handful of found footage movies come out after this disruptive original indie. So Paranormal Activity inspired countless imitators and a whole new genre while Blair Witch does not. Why?

Oddly, popularity has nothing to do with it. Nor do economics. It’s smart to expect those drivers: popularity drives the zeitgeist which drives filmmaker inspiration. And economics compel producers and studios to invest in new genres. But in reality, Blair Witch was more popular and economically successful than PA. Nominally, Blair Witch made $604M in the box office, which is a little more than PA. And if we adjust for inflation, Blair Witch made $1.3B by today’s standards. So it’s unlikely that economics or viewership made the difference.

At two different times, very similar movies are released, both to very large audiences, both extremely profitable. But the second one has a knock-on effect of inspiring copies and the other does not. When I give this lecture IRL, we stop here and mine for different theories from the class (and I’d be curious to hear yours too!). There is no right answer. However, my hypothesis is that one macro theme captures many of the drivers: technology lowered the barrier of entry for this type of filmmaking.

In the 10 years between 1999 and 2009 there were multiple technological developments in entertainment which make copy cats of PA far more viable. DV cameras spread with the Panasonic DVX100 and Canon XL2 introducing a “prosumer” category (and eventually DSLRs like the Canon 5D). Non-linear and prosumer editing software like Final Cut Pro gains rapid market share and becomes available to consumers at a lower price point (accelerated with piracy as distribution) plus iMovie is bundled with Macs in 1999. HD video becomes widely adopted which doubles the resolution of a home movie. Online distribution and promotion become possible through YouTube and crowdfunding platforms. I’d even argue that software and websites for staffing/coordination hit more of a stride around 2009 (craigslist, Celtx, MySpace). Even the more qualitative cultural changes (like normalization of UGC and shaky cameras) are dependent on these technologies’ proliferation.

Imagine trying to make Blair Witch before all of this. Editing a movie required a special combination of Avid software and hardware rented from a post house on a per-hour basis (the creator of Blair Witch had access to these computers through his day job). The Blair Witch filmmakers found their cast through an ad in a physically printed magazine. Even in its simple, “home movie” form, Blair Witch was intimidating to replicate.

Paranormal Activity’s impact isn’t just a story of creative inspiration; it’s an example of how technological accessibility plays a parallel role in trendsetting. In the years between The Blair Witch Project and Paranormal Activity, it took dozens of technologies across the filmmaking supply chain to unlock a new genre. As we consider AI’s potential in entertainment, I like to consider possibilities like this one. AI is poised to do for fringe content what DV cameras and non-linear editing did for found-footage. Yes we’ll lose some jobs but in those particular areas (VFX, stock footage), barriers to entry will come down and enable new talent. I predict we’ll see many more new genres proliferate, inspired by innovative boundary-pushers with the right timing. Just as we saw with found footage, by reducing production costs and creative limitations, AI will enable niche formats tailored to diverse audiences.

Thanks to Scott Brooks and Ryan Latchmansingh for reading drafts of this!

The guerrilla marketing campaign for Paranormal Activity could be its own case study. In trailers and on social media, ads asked fans to “demand” online that the movie come to their local theater. Then, as the movie spread to more screens, the ads showed off the number of new screens and proclaimed “you demanded it!” Trailers even utilized night vision footage of folks’ shocked reactions in theaters. Most likely, distributors had to commit to rolling out the movie nationwide months in advance because of the complexity of P&A– so the social proof of “you demanded it” was as much a hoax as the footage in the movie. ↩︎

I’ve been thinking a lot about the rumor of Apple’s hardware and content subscription bundle. The idea — whether it actually happens or not — is that they’d create a very expensive subscription of $80/month or so that bundles Apple Music, the new Apple original content, Apple Care, iCloud and a new iPhone every year. This is very much a rumor but very viable avenue posited here and by Matthew Ball at Redef.

This immediately reminds me that for years, Americans paid $100+ per month for another expensive hardware and content bundle: cable TV. I remember the salesman coming to my home and explaining to my parents what cable TV included. It was much more than TV, because before the internet, that box was your only gateway to many things. It was movies, music channels, educational programming for your kids, breaking news, live concerts and the hardware to make it all look beautiful on your only screen.

One way to frame Apple’s rumored hardware/content bundle is that they attract you with their device ecosystem (hardware) and then keep you hooked with their shows and music (content). The phone and its TV and cloud components are already a huge draw for audiences so their content can play the role of keeping users engaged there by making that ecosystem useful on a daily basis.

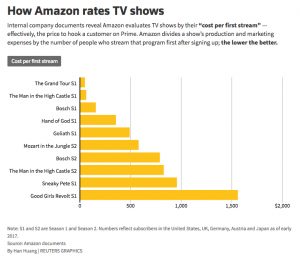

This got me thinking… maybe content isn’t really an effective audience awareness or acquisition tool AT ALL. Maybe, when all the cards fall, content is just the retention piece of a recurring payment business model and other elements of the bundle are what bring you in the door. This is somewhat reflected by the calculus Amazon did around their original video: it turned out that prestige TV shows like Mozart in the Jungle and Man in the High Castle weren’t such an efficient acquisition tool for Prime.

Check out how this thinking might apply to other businesses. I’ll use this analogy: come for X (acquisition); stay for content (retention).

Apple hardware/content bundle – Come for the hardware ecosystem; stay for Oprah.

Amazon Prime – Come for free shipping; stay for Nicole Kidman.

HQ — Come for a cash prize; stay for the trivia.

Facebook — Come for your friends; stay for Facebook Watch.

And the corollary seems to also be true with failed SVODs and streaming services — there’s no acquisition component, just a bunch of originals and licensed content to retain the audience that never came.

There are probably a bunch of examples that prove this thesis wrong, chief of which are Netflix and HBO. (But you could argue that they OVER spend on content, trying to force content into becoming an acquisition tool.)

Even if it’s only a little true, it’s a helpful thought experiment: what if you had to launch a streaming service WITHOUT using content to acquire an audience? You’d have to offer real utility to your users — some other valuable product or service that would attract them to your subscription. Apple already has that part figured out: the phone, the ecosystem. And on the content side of your business, brands like Marvel, leagues like the NFL and celebrities like Oprah wouldn’t be as valuable because you already have a giant draw for new users. If your content is only playing the role of retention, it doesn’t need to hit an attention-grabbing must-see fever-pitch. It can be much less ambitious. You can spend way less than Netflix.

Netflix is killin it and I continue to be bullish on their future. There’s one corner of the business I’m afraid they’re being just a little too pensive about: mobile.

This year, they’ve launched some of their first short-form programming and some new native portrait features in their mobile apps. But I’m afraid this won’t stop other mobile competitors — Google and Facebook — from locking them out of this critical piece of the entertainment pie. Now is the time for them to begin spending in the mobile content space and here’s how they should begin.

Why mobile is critical to Netflix

Let’s start with why Netflix should care.

There’s an obvious massive market of short form video consumption, well-proven by YouTube and Facebook. 34% of global internet video traffic is shortform. So, when Netflix says they’re competing with all forms of entertainment, this seems like an obvious adjacent area to pick up some additional engagement — whereas interactive, live and sports are much more of a moonshot.

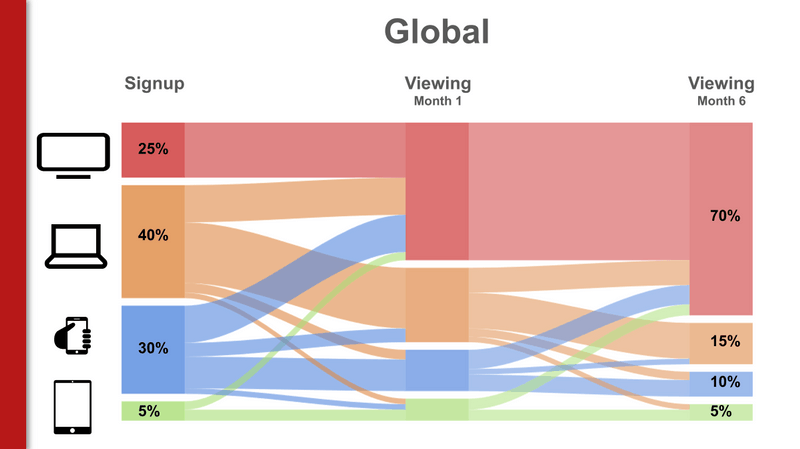

But I think all of that frames this as a business expansion opportunity when I actually think this is a threat to Netflix’s stranglehold on the streaming market. Have a look at this graph, which explains the userflow of new subscribers to the service.

When this slide first broke, a lot of emphasis was put on the fact that after 6 months, 70% of Netflix subscribers were watching on a big TV. What stands out to me is that 10% are STILL watching on a mobile phone. Just 1 month in, more than 15% are still struggling to watch long form TV shows and movies on a tiny mobile screen. And right from the getgo, a full THIRD of Netflix’s new users start on a mobile device.

We are in a mobile world and who cares that people watch more content on their mobile phones — people TRANSACT more on their mobile phones. Enough people subscribe to Netflix straight through iOS that they’re trying to bypass Apple altogether — another sign of just how many folks sign up on mobile. Given that Netflix’s model is dependent on one giant transaction at the top of the funnel (their subscription), many more of their new customers are entering their ecosystem through mobile phones. And this user flows shows just how long it takes that mobile customer to begin finding big-screen-TV-type-value in their subscription. Were Netflix to actually provide valuable mobile content during that couple-month transition, they’d reduce churn among new users. (Still another strategy would be a freemium model of mobile-only content to lure users through the paywall when they realize the app’s value on another screen.)

What Netflix is already trying in mobile

Netflix is not completely blind to this. They’ve launched a few new short-form originals and mobile products this year. For those trying to reverse-engineer their mobile content strategy, here’s a recap of their short form content:

The Comedy Lineup (15 minutes) – Mini stand-up comedy specials

Explained (14-18 minutes) – Newsmagazine (Vox)

Follow This (16-18 minutes) – Newsmagazine (Buzzfeed)

Comedians in Cars Getting Coffee (12-25 minute) – Celebrity interviews with Jerry Seinfeld

Marching Orders (12 minutes) – Docuseries

Cooking on High (14 minutes) – Competition reality

In the scheme of Netflix’s $6 billion content spend, I’d call this an extremely modest beginning — it’s really just a test. It’s heavy on news and unscripted, there are no filmmakers, high-value talents or standout IPs. I estimate their 2018 spend on short form around $20MM at most. To make a meaningful move into mobile, they’ll need to spend 5-10x that.

How Netflix could form a mobile content strategy

It’s clear that Netflix needs to get into the mobile content game ASAP. But how? So many short form content platforms from go90 to Watchable have flamed out because of a lack of distribution.

Broadly, I’d approach this similarly to the rest of Netflix’s business:

START FAST with a mountain of inexpensive mobile content that’s easy and fast to launch.

PIVOT TO PREMIUM – Use the analytics gathered from starting fast to inform a mobile Originals strategy and finance exclusive new series.

Why this two-part strategy always works is the subject of a whole other blog post. But Netflix is in a unique position to build a war chest of start-fast mobile content at a low cost-per minute without sacrificing their premium values. Step one of fast/easy/quick mobile content — pretty obvious — is licensing. Now is a fantastic time to cheaply license premium mobile content. Every mobile content studio is clamoring to work with Netflix which earns them outrageous leverage. Plus, many of them were gifted back go90 or other mobile series that they have no place to distribute. The second source of start-fast content is probably less obvious: the content they already have. Netflix outright owns a lot of their shows and by getting creative, they’ll find a new life if they’re re-cut for a shorter runtime or carefully cropped for a vertical screen.

When audiences coalesce around their start-fast mobile content, they can decide where it makes sense to pivot to premium, maintain licenses or trim back.

In sum, I think mobile is a crucial growth area for Netflix and a place they have some natural competitive advantages. They could quickly turn a source of churn into a new source of revenue and expansion. I predict they’ll make some dedicated moves in this space but it’s going to take a larger commitment to realize the potential mobile content has in Netflix’s future.

I love how ballsy this would be. Disney is out of Netflix and has announced their plans to make a similar service. And in a guest post on THR, Ben Weiss posits this crazy new move: that Disney could quickly amass a big subscriber base by launching their movies on the service “day-and-date” — that’s the much-feared-by-theaters idea that a movie could be streamed the same day it releases in theaters.

It’s brilliant because it endruns the entire traditional entertainment distribution-windowing business model in favor of the consumer preference of when-I-want-where-I-want. It would definitely grow them a huge base of subscribers. But they’ll never do it.

Disney is already giving up $300 million in revenue by opting out of Netflix.

Theatrical is the majority of their studio entertainment revenue, about 60%… and a move like this wil piss of theaters and threaten that nut. Theaters may refuse to carry the movies or put them in fewer cities. It may even piss off some consumers who still like the theater experience– if their local chain decides not to carry the movies over this move.

If Disney does day-and-date they’re not just threatening the theatrical revenue. They’re endrunning all of their studio ent distribution: pay TV, home entertainment, etc. Why would another provider value their content the same way if it’s already debuted in a streaming window?

And finally, the REAL business of Disney is parks and products — maybe twice the revenue of all of the studio business. What if this slow, gradual windowing model actually helps propel their brands in those venues? It might be a stretch but my instinct is that being in every theater in America is the best billboard ever for a parks attraction or action figure. Better not mess with that.

But, boyyyy, would I love to live in a world where studios made distruptive moves like this. I dare you, Bob!

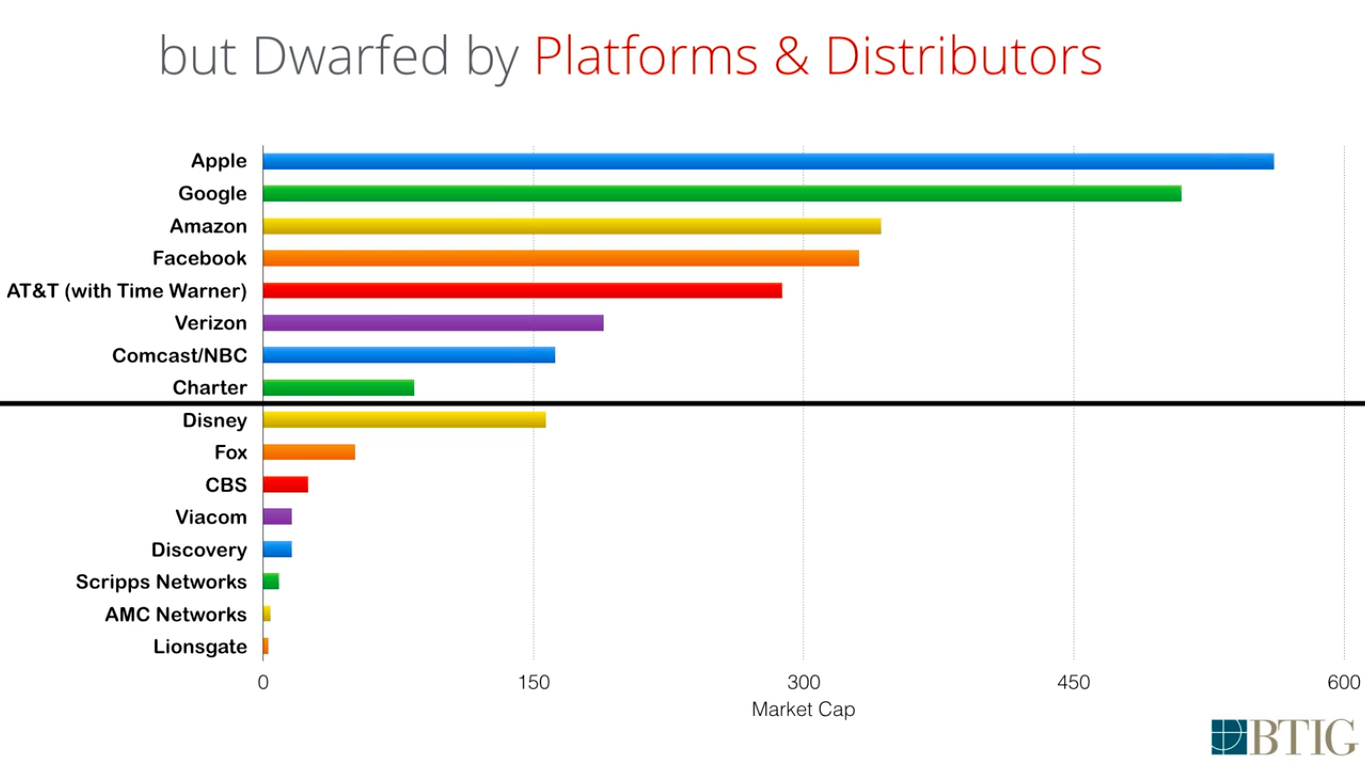

I LOVE LOVE LOVE this slide from Rich Greenfield at BTIG. His whole presentation is definitely worth the watch but this one graph truly says it all. (And I’m always trying to pull it up online to share in meetings… so I’m also posting it here to make that much easier.)

In the presentation, Rich first shows market caps of the companies below the line — all of our beloved entertainment creators. We see them in print and on every screen and think of them as massive, powerful companies. Then, he layers on the market caps of the “platforms” and distribution companies that sit between those companies and their audiences… and it’s easy to see how those content co’s are dwarfed.

Rich is looking at this through almost exclusively through a lens of financial analysis and market value… which might not tell the WHOLE story, but it paints a pretty dim picture for content creators and brand owners: Content is not king.

Some things worth noticing (many of these points are made by Rich):

None of the entertainment companies below the line — even the juggernaut, Disney — has a meaningful direct-to-consumer platform… they all depend on the companies above the line to reach their audiences

Apple could buy Disney in cash

Google or Apple could buy the entire entertainment industry in cash, except Disney

Every one of the distribution companies above the line have meaningful plans to make their own content that they own completely and perpetually (in other words, they could start to make their own content without depending on the content companies and their brands)

Netflix isn’t even on here but its market cap around $70B, making it bigger than everyone but Disney

Neither is Snap… it’s much smaller than Netflix at $20B (as of this writing), but it still stacks up above Viacom, Discovery and others

The digital-oriented distributors like Facebook, Apple, Google and Amazon have incredible volumes of data and knowledge describing their audiences, which is a huge advantage in content creation

While some of the content companies have partnered with and invested in the FANGS companies, they’ve missed their chance to buy one of them or build their own; Hulu is the only example and they half-heartedly participate in it

Nobody has been able to successfully create a large “direct to consumer” platform with content or brands alone… Netflix had to use DVD rentals, Amazon is using ecommerce, Spotify is using music and UI. In other words, we haven’t seen someone earn lots of subscriptions and ad revenue by only saying “we have ESPN.” It’s always content paired with some other strategy.

What Rich calls the “punchline” is this great thesis: content companies — especially Disney — have to make an acquisition in order to complete their business. What should they buy? Well, all of their options SUCK. Netflix is too expensive. Snap and Twitter don’t come with subscriptions. Pandora or Spotify aren’t video platforms.

That punchline explains many of the plays we see being made around the industry: Twitter continuing to pursue video in an attempt to demonstrate its value as a video platform. Time Warner selling itself to AT&T. Netflix spending billions on original content. NBC investing heavily in Snap. The list goes on…

I’m finished with college. Next semester, I’ll be taking yoga and independent studies. It ought to be a hoot.

But my capstone presentation was about web video distribution. Appropriately, I streamed it online. About 50 people were in and out during the live stream and hopefully they were all thinking, “I can’t wait to hire this kid in May!” Maybe not.

I’m especially proud of a concept I’ve engineered called “segment parsing.” I introduce it in the video — but there’s more to come soon.